How entrepreneurship is changing

1. Prior to the pandemic, formation of new employer businesses had been in a longterm slowdown, with startup rates declining slightly faster in Minnesota than the U.S.

Minnesotans are creating fewer new employer businesses than in past decades. The state’s falling business formation has largely mirrored the national trend line, though the decline is somewhat steeper in Minnesota than the U.S. as-a-whole.

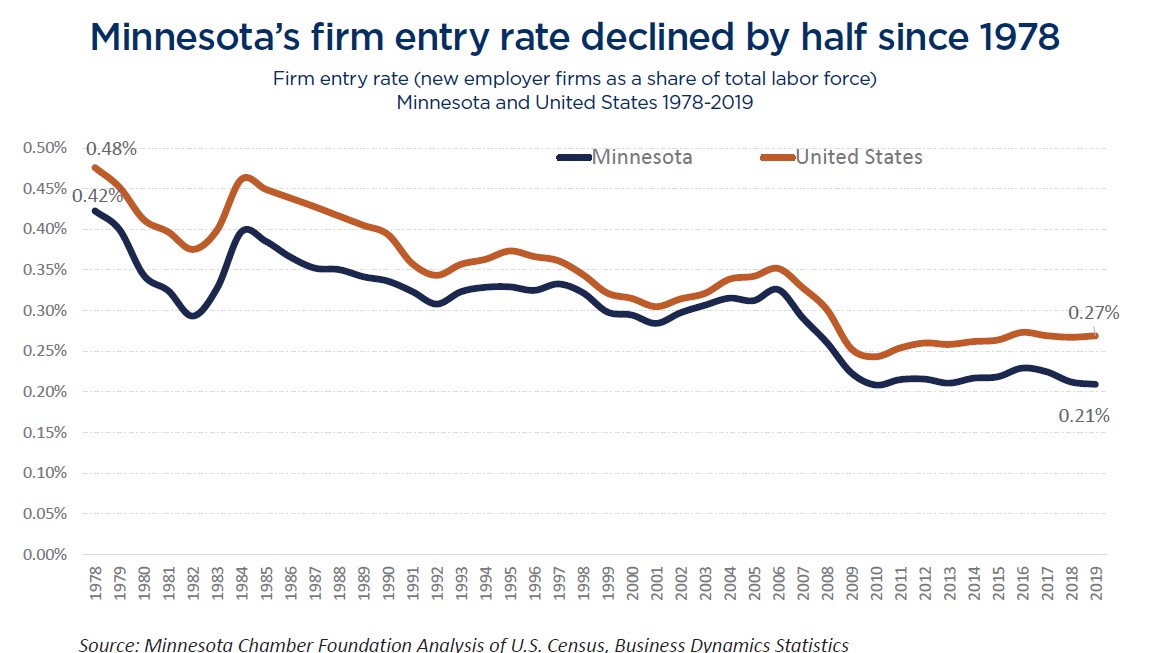

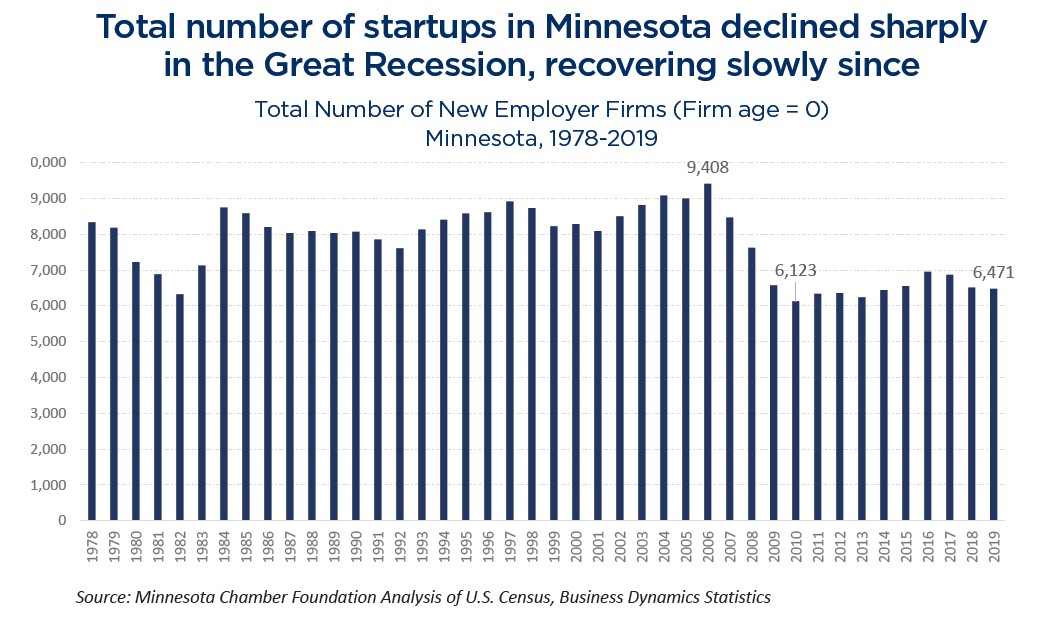

Minnesota’s firm entry rate (i.e. new employer firms as a share of the total labor force) fell by half from 1978 to 2019. This decline worsened after the 2008 Great Recession and business formation has recovered only slowly since then, widening the gap between Minnesota and the rest of the nation. From 2008 to 2019, Minnesota averaged 6,585 new employer firms a year, down from an average of 8,214 annually over the prior three decades. This amounts to roughly 1,600 fewer new employer companies forming in Minnesota each year compared to the long-term average.

Startup job creation also fell alongside the overall drop in new business formation. Minnesota startups created 48,000 jobs a year on average in the three decades from 1978 to 2008. Since 2008, however, startup job creation fell to an average of 38,000 new jobs per year. This reduction in startup job creation appears to be caused by fewer new businesses forming rather than fewer jobs created per startup. Indeed, the number of jobs created per startup remained relatively stable in recent decades.

In 2019, Minnesota even reached a 42 year high with startups creating an average of 7.4 new jobs per firm.

The bottom line: heading into the 2020s, Minnesota had been producing fewer new companies than in past years, creating a drag on the state’s overall economic performance.

The decline in new employer business formation over time is a well-documented phenomenon. But what is causing this decline in the first place?

Factors influencing declining business formation:

Economic research on firm formation suggests that population growth is an underlying condition of entrepreneurship, creating both supply and demandside incentives for new businesses. The long-term decline in business formation in the U.S. has been linked to slowing population growth in recent decades. As economists Ian Hathaway and Robert Litan state:

“The relationship between regional population growth and firm formation rates is remarkably strong, even after controlling for other factors – including unobserved time and regional effects (such as industrial and labor market composition, culture and potentially, public policies).”

The same is evident in regional and state variations in entrepreneurship, with startup activity increasing in states with the fastest population growth.

Closely related, new businesses require available workers who can help them grow and scale their operations. Research from the Federal Reserve Bank of San Francisco showed that a 1% increase in the number of workers was associated with a 1% increase in the number of new businesses at the state level, with labor availability accounting for 90% of variation in new business starts over time and across states. This is a concern, as workforce availability challenges have only increased in recent years. As one founder relayed in a focus group, “the talent piece is even more difficult than the funding piece.”

Additionally, local and state policies may play a role in incentivizing or discouraging startup activity. Economists find that young firms are particularly sensitive to changes in state corporate tax rates and less able than larger firms to absorb high fixed costs. Corporate tax rates are negatively correlated with startup job creation and act as a drag on new business growth.

As argued elsewhere, Minnesota has among the highest tax rates across multiple categories, creating concerns for the state’s long-term competitiveness. Addressing these structural factors are the necessary precursors to fostering long-term growth in new business formation.

2. States in the Sun Belt and Western regions have seen the largest relative startup gains, while states in the Midwest and Northeast have seen the largest declines.

One of the major shifts in American life over the past half century has been the steady migration of people to Western and Sun Belt states. Since 1970, population grew by 126% in the West and 101% in the South compared to just 22% in the Midwest and 17% in the Northeast. While growth rates are slowing in all regions of the U.S., western and Sun Belt states continue to experience a higher relative share of economic and population gains. Not surprisingly, these same trends have shaped regional variation in startup activity.

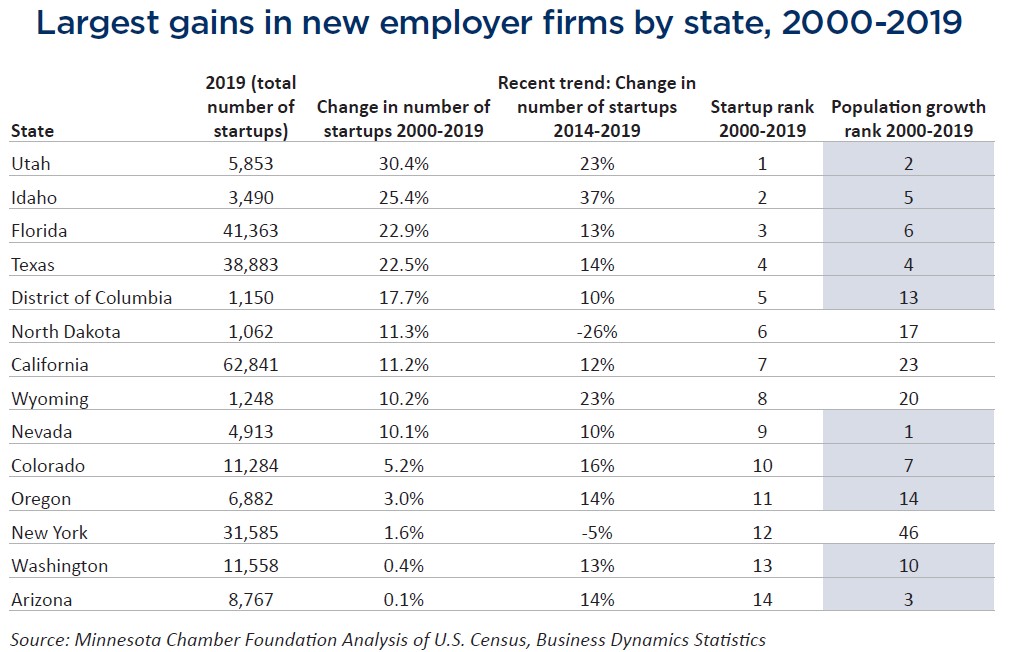

Since 2000, only 14 states (and Washington, D.C.) experienced an increase in their total number of employer startups. The remaining 37 states experienced overall declines in new employer firms. Of the 14 states with an increase in new startups, four of them are the nation’s largest states: California, Florida, New York and Texas. These four states alone make up one-third of the U.S. population and accounted for 40% of all U.S. startups and 40% of startup job creation from 2013 to 2018. Other states with increasing startup levels include those with above-average population growth and overall economic growth – again, predominantly (though not exclusively) in Western and Sun Belt regions.

Minnesota ranked 40th among all states in the change in new employer firms from 2000 to 2019, with the state producing 22% fewer new companies in 2019 than in 2000. States with the steepest declines in startups were concentrated in the Midwest, Northeast and interior South.

3. Entrepreneurship is shifting from employer to nonemployer firms over time.

Fewer people are starting new businesses with paid employees than in past decades. This does not, however, necessarily mean that the population has become less entrepreneurial overall. The U.S. selfemployment rate (i.e., the share of the population whose primary income comes from their own business) has remained relatively stable in recent years. The same is true in Minnesota. In 2019, nine out of every 100 Minnesotans were self-employed, down by just one percent from 2010. So, if roughly the same share of the population is self-employed, how is it that business formation is in decline?

The answer lies in part by the types of ventures that entrepreneurs are forming. As economist Lyman Stone states:

“Fewer new businesses are forming. This is not because Americans are no longer coming up with ideas or because they have no entrepreneurial spirit. Americans are filing business income, starting nonemployer businesses, and identifying as freelancers, as much as they ever have. They just cannot seem to turn these ideas into thriving businesses that employ people.”

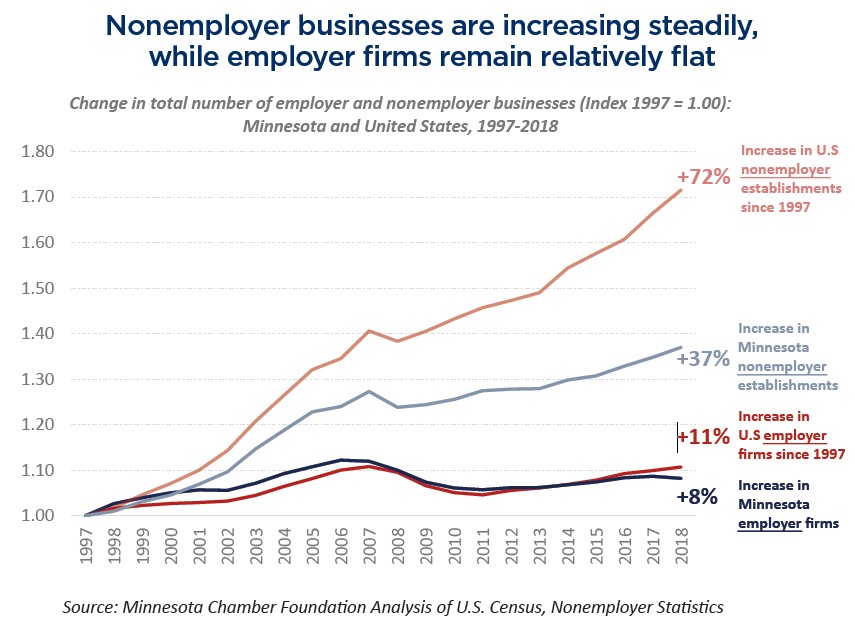

This shift is evident by looking at the change in the total number of employer and nonemployer businesses in operation over time. Since 1997, the total number of nonemployer businesses increased by 72% in the U.S., compared to an increase of only 11% for employer firms. Minnesota experienced the same basic pattern, but with the number of nonemployer businesses increasing at roughly half the rate of the U.S. Thus, while Minnesota lags the U.S. just slightly in new employer firms, the gap in the formation of nonemployer businesses is much starker.

This presents a set of trade-offs for Minnesota’s economy. First, while nonemployer businesses make up roughly 80% of all firms in the United States, they generate just 3% of total annual business receipts.

They are also muchmore likely to be self-financed, and many do not seek to scale and grow in a substantial way, being motivated instead by lifestyle factors or necessity.

This is not true of every nonemployer business, of course. Many high growth startups begin as small nonemployer ventures before taking the next step of raising capital, scaling operations and adding employees. But on the whole, only a small subset of nonemployer firms fit this description. The risk for Minnesota, however, is that fewer nonemployer businesses means a smaller pool of entrepreneurs who can potentially succeed and take their business to the next level. As stated in a Small Business Administration (SBA) report, “Nonemployers are important in creating the stock of businesses from which employers arise; in providing learning opportunities for future businesses or expansions; and in generating flexible work options, economic cushion, and empowerment.”

Indeed, states with a higher number of nonemployer businesses per capita tend to also have more employer startups per capita.

In short, the growing prevalence of nonemployer businesses creates both opportunities and risks for Minnesota’s economy. Supporting measures to encourage more broadbased entrepreneurship may help create a larger pool of businesses with the ability to scale and offer economic opportunities to entrepreneurial-minded individuals. Yet, to maximize the economic impact of such efforts, entrepreneurs will require the resources, technologies, and, whenever appropriate, the personnel needed to grow their business to its full potential.

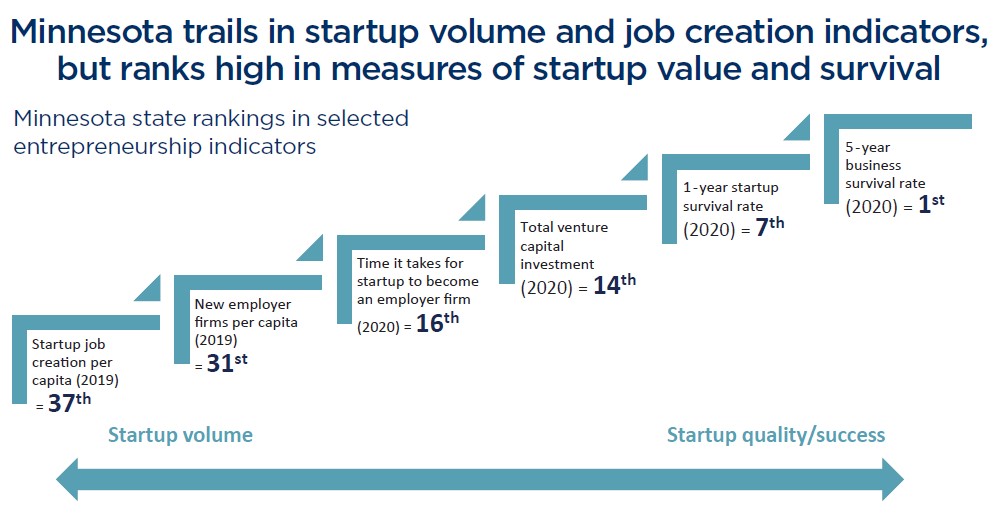

4. Startups in Minnesota get off the ground faster and survive longer than peers in other states.

Each year, the Kauffman Foundation releases two companion reports assessing eight key indicators of entrepreneurship for each state in the U.S. As these reports reveal, Minnesota consistently ranks below-average in the rate of new business formation, as measured by both the share of the population that starts a business of any kind (rate of entrepreneurship indicator) and the number of new employer businesses per 100 people (rate of new employer businesses indicator).

However, these reports also reveal that despite the state’s lower volume of startup creation, Minnesota entrepreneurs are more likely to turn their ideas into businesses that employ others, and they make that transition faster than entrepreneurs in most other states. Minnesota ranks 16th in the time that it takes for a new business application to become an employer firm and ranks 17th in the share of new business applications that become employer businesses within eight quarters. In other words, once an entrepreneur files a new business application with the federal government to receive an Employer Identification Number (EIN), it takes them less time to get their business off the ground and make payroll. This is important because the economic impact of startups relates largely to whether they turn into more established businesses that innovate, add jobs and scale beyond their initial stage.

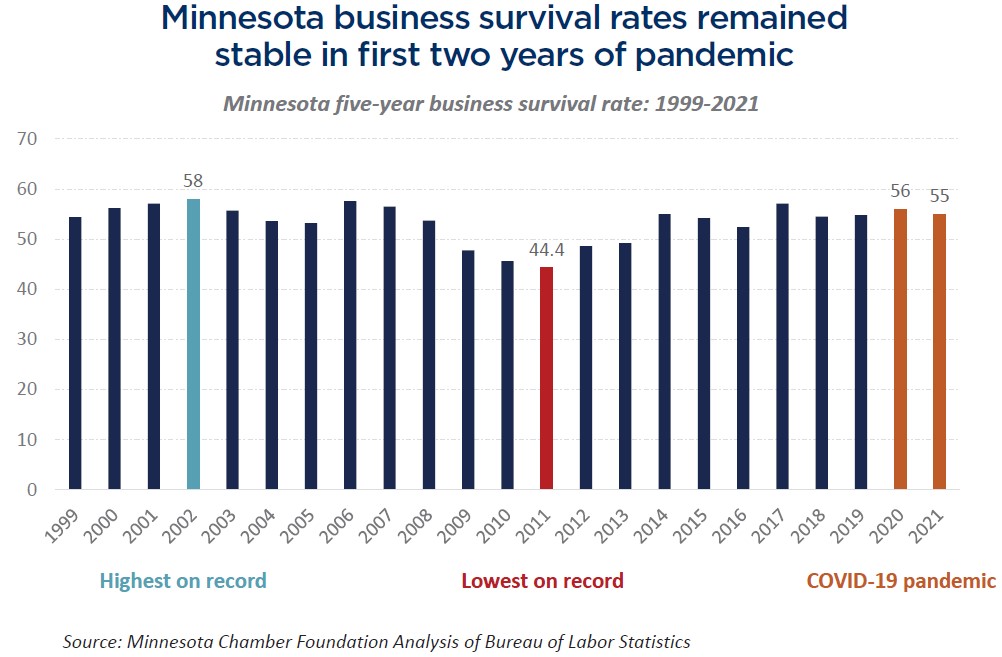

Data from the Bureau of Labor Statistics also show that Minnesota has among the highest business survival rates in the nation. Minnesota ranked 7th among all states in one-year startup survival and had the highest five-year business survival rate in the U.S. in 2020. The state’s high business survival rates have been stable over time, proving this to be a durable attribute of entrepreneurship in Minnesota. This was true even in 2020 and 2021, as the COVID-19 pandemic brought about unprecedented challenges and disruptions for businesses of all types.

With fewer businesses failing in their first five years, Minnesota should theoretically have higher firm concentration and employment levels relative to other states for firms in their fifth year compared to the population of firms in their first year. This indeed appears to be the case.

Minnesota ranked 31st in new employer startups (i.e. firms age = 0) per capita in 2019, but had the 25th highest concentration of firms aged five. Similarly, Minnesota ranked 37th nationally in jobs per capita for startups in their first year but ranked 28th for jobs per capita for firms in their fifth year. Minnesota’s national standing moves from the bottom third of states to the middle of the pack over a five-year period, demonstrating the impact of its higher survival rates.

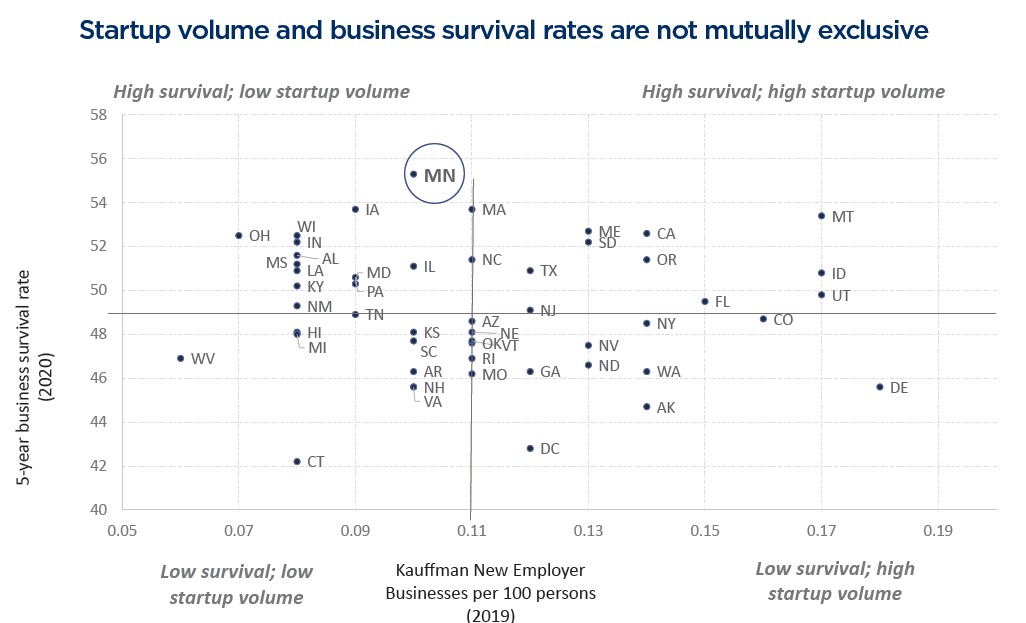

Despite these strengths, however, a note of caution is warranted. It is not the case that states must settle between either high startup rates or high business survival rates. These two attributes are not mutually exclusive. States like California, Montana, Oregon, Idaho and Utah combine above average five-year business survival rates alongside above average rates of employer startup formation. At the other end of the spectrum, states like West Virginia and Connecticut rank particularly low in both indicators. Minnesota could seek to accelerate the number of new startups without necessarily reducing the quality and longevity of these new ventures.

In short, Minnesota’s startup formation rates lag slightly behind the national average, but the companies that do start here are more likely to become employer firms and survive longer than startups in other states. This produces a modest catch-up effect, as fewer firms fail and continue to yield economic benefits over time. At the same time, Minnesota has an opportunity to accelerate new startups without necessarily losing its advantages in actualization and survival.

5. High growth startups are a Minnesota strength, and there is positive momentum on this front.

New businesses are vital to the economy. They are also volatile, however, with nearly half of all new firms failing in their first five years. Even among those who survive, most businesses remain small and grow at a moderate pace over the course of their life span.

The research literature on entrepreneurship shows an “up or out” phenomenon where a small sub-set of all new businesses contribute a disproportionate share of job creation, output and productivity growth.” These “high-growth” firms are an important component of Minnesota’s entrepreneurial landscape and future economic growth.

Fostering businesses with high-growth capacity has long-been a strength in Minnesota. This is demonstrated by the presence of home-grown industry clusters and notable headquartered companies that began as startups in Minnesota and sustained their growth here over time. The question is, who are the next wave of innovative new companies with the capacity to scale and shape Minnesota’s economic future?

History shows that successful companies can emerge across a wide range of industries and take various pathways along their growth journey. There is no one-size-fits-all model.

Yet venture capital activity provides one way to assess the subset of Minnesota startups that intend to scale and are raising growth capital to do so. Venture capital-backed firms are more likely to succeed and contribute disproportionate gains to the overall economy, making them a good proxy for high growth-potential businesses. There is good news for Minnesota on this front.

Venture capital investment is on the rise in Minnesota:

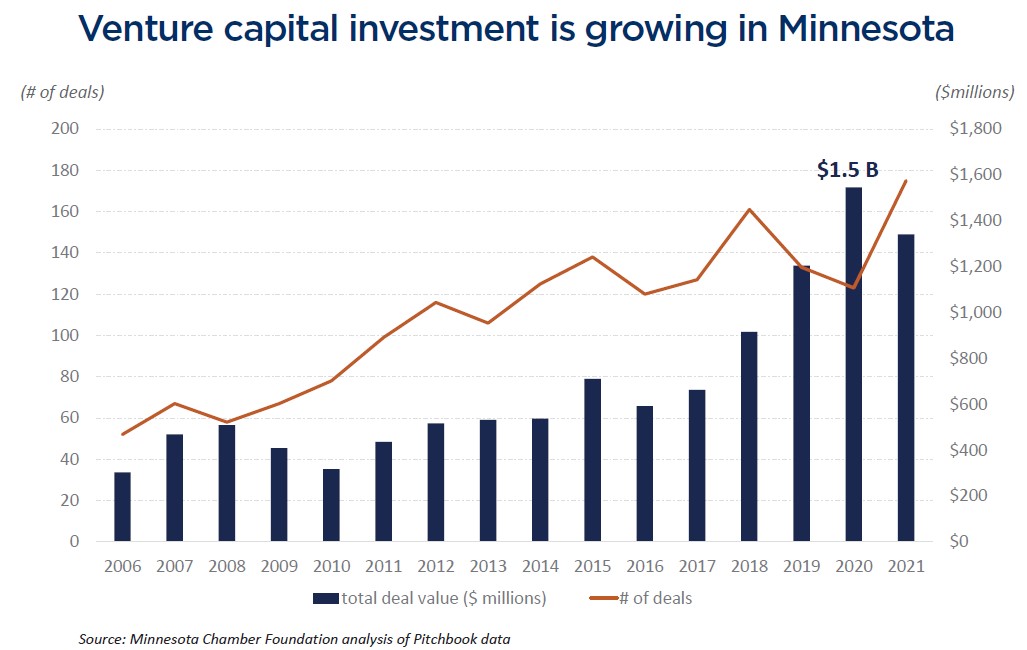

Data from Pitchbook – a leading database tracking investments in private capital markets – show that venture capital investment surged in Minnesota over the past five years, following broader national trends.

The COVID-19 pandemic only accelerated this trend. Minnesota startups raised a record $1.5 billion in venture capital in 2020 and reached a record 175 deals in 2021. This demonstrates both the rising value of startup investments as well as a broadening base of startups that are receiving venture capital.

Minnesota ranks relatively high among states in total venture capital investment. Despite having the 22nd largest population, Minnesota typically ranks in the top 15-18 states for total venture capital raised. Further, Minnesota experienced the 7th fastest growth in total VC raised from 2015-2020 among states with at least $1 billion in total deal value. So while the state’s overall business formation rates may lag the U.S. average, the opposite is true when narrowing the focus to startups with high growth potential.

Minnesota continued to broaden its base of companies raising venture capital in 2021 but did not experience the same wave of deal value that flooded the U.S. market last year. Venture capital roughly doubled in the U.S. in 2021, with some states experiencing 3x or higher growth. However, interviews with local venture capital leaders suggest that the longer term trend line may be a more meaningful indicator of the state’s performance, as year-to-year changes can fluctuate largely based on the timing of investment rounds of just a handful of companies. Additionally, Minnesota’s broadening base of startups raising capital may be just as important, or more so, than deal value alone.

In short, investors are putting more dollars behind more Minnesota startups to innovate and scale in the near-term.

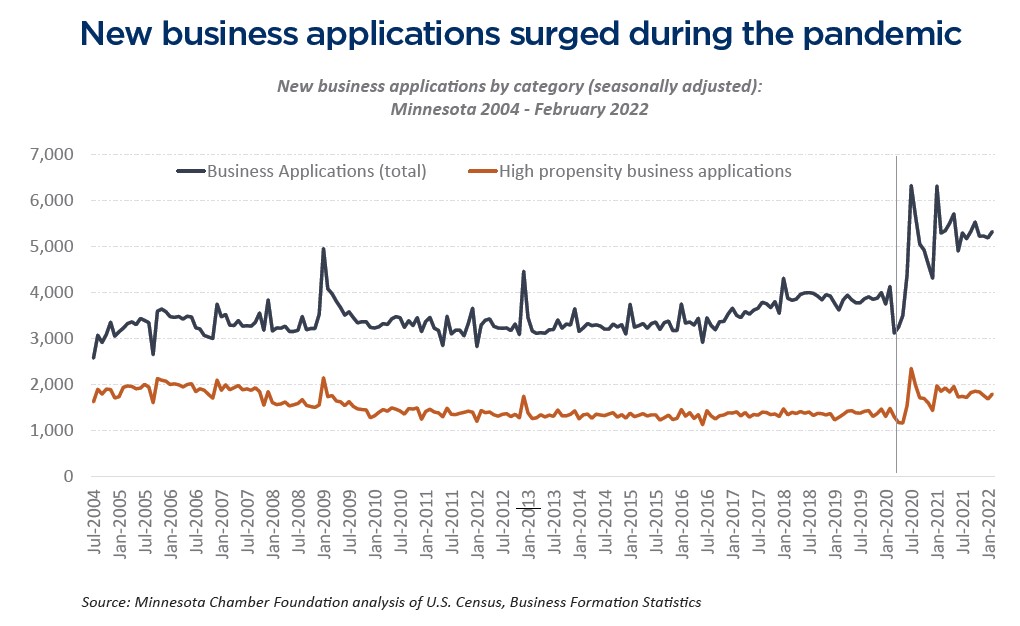

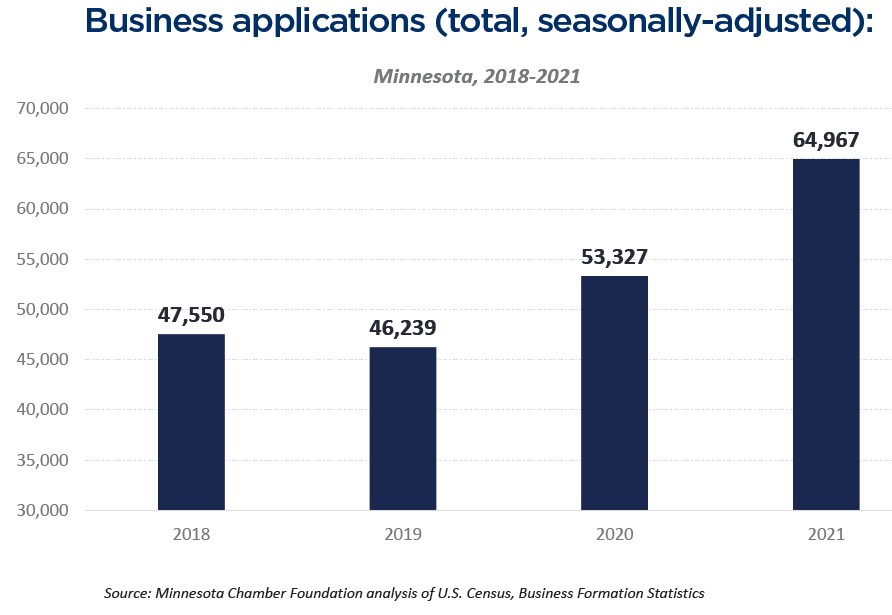

6. New business applications spiked during the pandemic both nationally and in Minnesota, presenting opportunities for the near term.

One of the most surprising outcomes of the COVID-19 pandemic has been the sudden and dramatic surge of entrepreneurial interest. The U.S. Census tracks month-to-month changes in new business applications through its Business Formation Statistics data series. These data show that new business applications rose by a staggering 39% in the U.S. in the first two years of the pandemic (2020 and 2021) compared to the prior two years of 2018 and 2019. New business applications have remained elevated throughout the pandemic, suggesting that the change reflects more than a one-time aberration. This same shift is taking place in Minnesota as well. Minnesota business applications rose by 26% in 2020 and 2021 compared to the prior two-year baseline. Encouragingly, this rate of increase was also high for the subset of applications that the U.S. Census designates as “high-propensity,” meaning that they are likely to become employer businesses based on one or more criteria in their application. High propensity applications increased by 22% in the first two years of the pandemic in Minnesota, compared to 24% nationally. Thus, while Minnesota lagged the U.S. average for total business applications by a larger margin, the state roughly mirrored the national rate of increase for likely-employer firms. This is an encouraging sign for the near term.

Temporary blip in the radar or start of a longer-term shift?

New business applications are only a leading indicator of potential new business starts – they represent the intent to form a business rather than the actualization of a new business. It remains to be seen whether this spike in entrepreneurial interest will translate to an actual rise in new business starts. It is possible that factors unique to the pandemic will prevent these potential startups from coming to fruition.

However, research shows that new business applications are a reliable predictor of new business formation. This suggests that – barring some reversal in the relationship between new applications and new businesses – Minnesota and the U.S. are poised to experience at least some level of increased startup activity in the near term.

Whether this current surge sustains beyond the short-term remains an open question. Structural factors like slowing population and labor force growth may return business formation levels to their pre-pandemic sluggishness in the years to come. However, countervailing forces such as technological changes and shifting attitudes around work could potentially mark the beginning of a sustained resurgence in entrepreneurship.

Data on new firm formation for 2020 will not be released by the U.S. Census until late 2022. But these lags in the data do not preclude communities everywhere to begin responding to this opportunity by broadening their efforts to support and fuel entrepreneurial growth.

Navigate the report

DOWNLOAD THE REPORT